How to Manage Money Better for Beginners — Practical Steps That Actually Stick

Most money management advice sounds obvious in theory and falls apart in practice. That’s because the advice isn’t wrong — the implementation is missing. This guide focuses on what actually works when you’re starting from scratch.

Why Most People Struggle With Money Management

It’s rarely about income. People earning $30,000 and $130,000 can both struggle with money management for the same reasons: no system, emotional spending, and no clear picture of where money actually goes.

The fix isn’t earning more (though that helps). It’s building systems that work with how you actually behave.

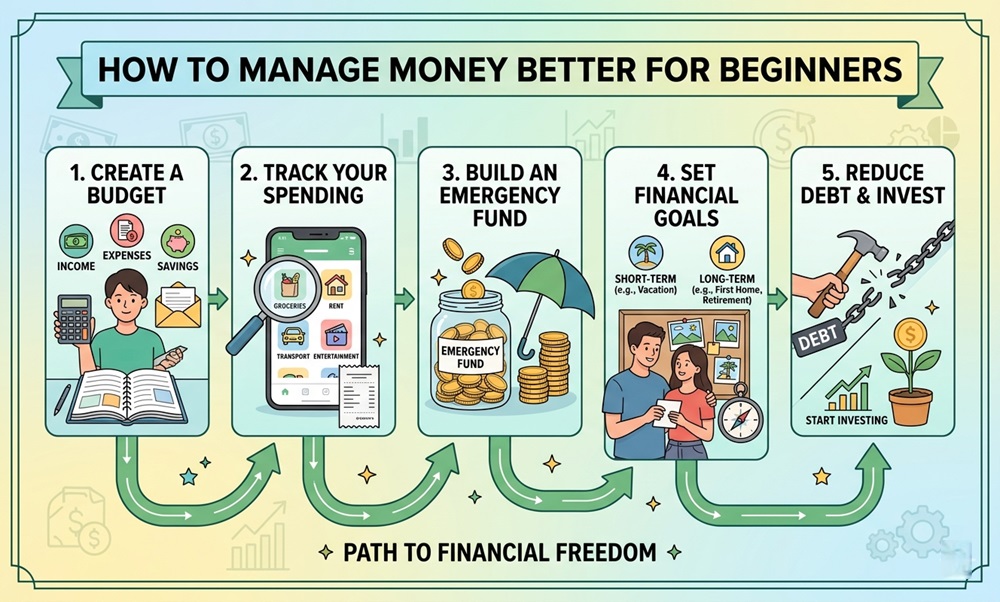

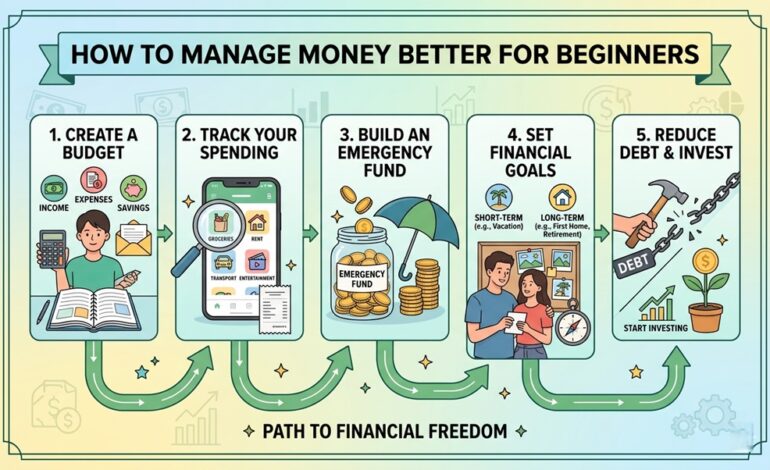

Step 1: Know Exactly Where Your Money Goes

Before you budget, you need data. For 30 days, track every expense — not to judge yourself, just to see the numbers.

Use any free tool:

- Your bank’s built-in categorization

- A free app like Mint or YNAB’s free tier

- A simple spreadsheet

Most people discover 2–3 categories where spending is significantly higher than they expected. That’s your starting point.

Step 2: Build a Budget That You’ll Actually Use

The 50/30/20 framework is simple and works for beginners:

- 50% — Needs: Rent, utilities, groceries, transport

- 30% — Wants: Dining out, entertainment, subscriptions

- 20% — Savings & debt repayment: Emergency fund, investment contributions, loan payments

If 20% savings feels impossible, start with 5%. Something is better than nothing, and the habit matters more than the amount at first.

Step 3: Automate Your Savings

The biggest reason people don’t save: they wait to see “what’s left” at the end of the month. There’s never anything left.

Fix: Move your savings contribution to a separate account automatically on payday, before you have a chance to spend it. Treat savings like a bill — non-negotiable.

Even $50/month automated is better than $300 saved manually “when you remember.”

Step 4: Deal With Debt Strategically

If you have debt, prioritize it in one of two ways:

Avalanche method: Pay minimums on all debts, put extra money toward the highest-interest debt first. Saves the most money mathematically.

Snowball method: Pay minimums on all debts, put extra money toward the smallest balance first. Builds momentum and motivation.

Choose based on your personality. The right method is the one you’ll stick to.

Step 5: Build an Emergency Fund

Without this, every unexpected expense becomes a debt situation. Target 3 months of essential expenses in a high-yield savings account (currently earning 4–5% APY at many online banks).

Common Mistakes to Avoid

- Building a perfect budget but never reviewing it — Budgets need monthly check-ins to stay useful.

- Not accounting for irregular expenses — Car registration, annual subscriptions, birthday gifts. These aren’t surprises — add them to your budget.

- Restricting spending too aggressively — Extreme budgets break. Build in a discretionary “fun money” category.

- Having only one bank account — Separating checking, savings, and an emergency fund prevents accidental spending.

Expert Insight

The habit that changes everything for most beginners is the weekly money check-in. Ten minutes every Sunday, looking at what you spent the week before and what’s coming up. It sounds small, but that awareness is what separates people who drift financially from people who make steady progress.

Simple Money Management Checklist

- Track every expense for 30 days

- Choose and set up a budget (50/30/20 or custom)

- Automate savings contributions on payday

- Set up a separate high-yield savings account

- Do a 10-minute money review every week

FAQs

Q: What’s the best budgeting method for beginners? 50/30/20 is the easiest starting point. As your situation gets more complex, you can refine it.

Q: How do I stick to a budget? Make it realistic from the start. A budget that allows no fun is one you’ll quit within a month.

Q: Should I save or pay off debt first? Build a small emergency fund ($1,000) first, then focus on high-interest debt aggressively, then continue saving.

Q: How much should I have in savings? Start with $1,000 (mini emergency fund), then build to 3–6 months of expenses.

Q: What if my income is irregular? Budget based on your lowest expected monthly income. When higher months come, funnel the extra into savings or debt.

Conclusion

Better money management isn’t a personality trait — it’s a set of systems. Track your spending, set a simple budget, automate savings, and check in weekly. These four things, done consistently, will change your financial trajectory more than any single tip or app. Start this month, not next month.